The development and implementation of central bank digital currencies (CBDCs) worldwide has become a topic of heated debate.

Proponents believe CBDCs represent the evolution of money. But critics say they are a possible tool of financial “surveillance.” Especially critics here in the US, where the Federal Reserve is testing a potential “US Digital Dollar” with several major banks.

In favor of the Digital Dollar’s development, Fed Chief Jerome Powell says, “the Fed is charged with the safety and efficiency of payment systems,” and by “embracing innovation” the Fed can help ensure “safer financial transactions.”

And according to an IMF Finance & Development staff member, leading experts believe CBDCs offer “greater resilience for domestic payment systems and foster more competition, which may lead to better access to money, increase efficiency in payments, and in turn lower transaction costs.”

However, the IMF also expresses concerns over CBDC transaction safety, saying, “Central bank digital currencies … also come with new and significant risks, particularly around cybersecurity and privacy.”

Why? Because CBDCs are programmable “virtual money.” So, they only exist as lines of computer code.

And unlike cash, this new “virtual money” may be vulnerable to cyberattacks. Which, according to a report by the Congressional Research Service, “could pose systemic risk and adversely affect the ability of the Federal Reserve and other central banks.”

But possible cyberattacks are just one side of the CBDC equation.

What about possible privacy risks?

Proponents are quick to point out digital banking technology is nothing new. After all, digital payment platforms like PayPal, Venmo and Cash App have existed for years, right?

True, but here’s the crucial difference:

CBDCs and the potential Digital Dollar aren’t digital payment platforms.

They’re not banking portals for sending and receiving money.

Instead, they’re a new form of digital legal tender tied to the central bank. And since our central bank, the Fed, would issue, control and monitor every CBDC or Digital Dollar transaction, critics warn this could invite unwarranted financial surveillance.

And for a very vocal group of representatives on Capitol Hill, the theoretical loss of financial privacy and freedom is their main concern.

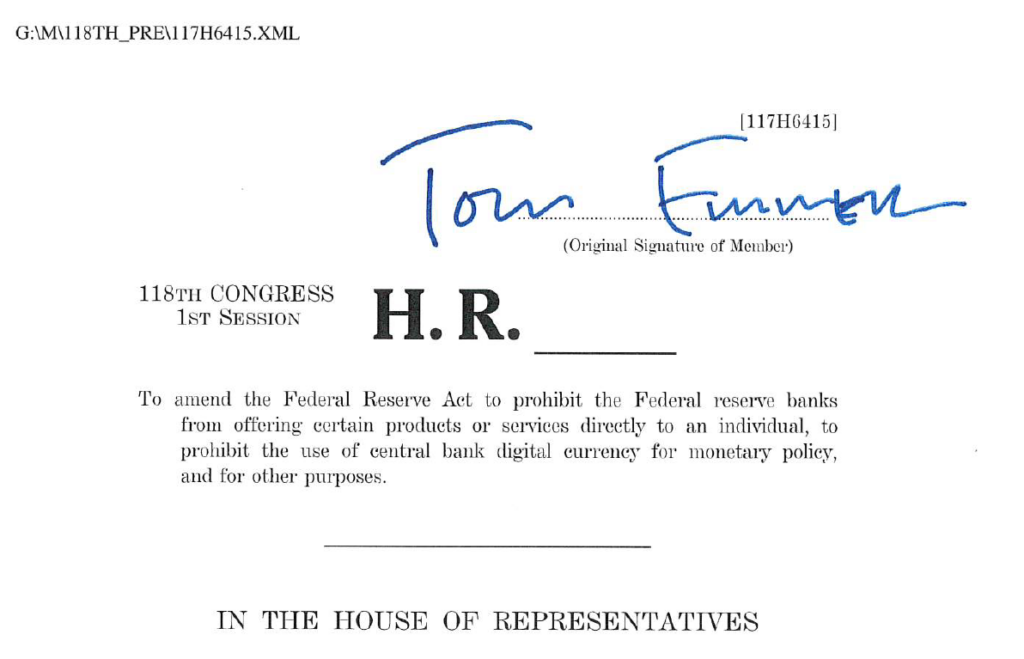

In February 2023, US Congressman Tom Emmer (R-MN) introduced bill H.R. 1122 called the “CBDC Anti-Surveillance State Act.”

And in his official press release, entitled “Emmer Leads Effort to Squash Financial Surveillance State Initiatives,” Congressman Emmer says the purpose of the bill is to “halt efforts of unelected bureaucrats in Washington, D.C., from issuing a central bank digital currency (CBDC) that strips Americans of their right to financial privacy.”

Commenting on his support for the bill, Congressman Pete Sessions said he was “very concerned that a digital dollar would fundamentally reshape the banking industry to the detriment of consumers and the economy, therefore Congress must fully consider the negative and unintended consequences that could result from issuing a digital dollar.”

Congressman Andy Biggs agreed and said, “A government-run digital currency presents a real threat to Americans’ freedom to use their hard-earned money, and fundamentally, to the value of that money.”

And Rep. Kim said he believes “the key to unlocking America’s economic future” is not a CBDC but “innovation.”

To help address concerns like these and encourage responsible development of CBDCs worldwide, the experts at the Atlantic Council created a comprehensive online “CBDC tracker.”

And according to the tracker’s interactive database:

The need for transparency and rational debate is urgent because:

- Right now, 114 countries — representing over 95% of global GDP (Gross Domestic Product) — are in some phase of CBDC exploration.

- All G7 economies — the United States, Canada, the United Kingdom, France, Germany, Italy, Japan and the European Union — are experimenting with and developing a CBDC.

- 11 countries have already launched their digital currency.

- And China’s digital yuan pilot project is now expanding to most of the country.

As you may already know, China is a member of the BRICS de-dollarization coalition along with Brazil, India, South Africa and Russia.

And remarks by Alexander Babakov, Deputy Chairman of the Russian State Duma, at the recent International Economic Forum event in New Delhi, India, indicated BRICS is also developing the BRICS digital currency in a cooperative effort to bypass the US dollar.

Babakov said the digital currency’s “composition should be based on inducting new monetary ties established on a strategy that does not defend the U.S.’s dollar or euro, but rather forms a new currency competent of benefiting our shared objectives.”

But here’s the interesting part…

The India Times says Babakov also “reportedly indicated the new BRICS currency would be secured by gold and other commodities…”

The US Digital Dollar, on the other hand, would remain a fiat currency — not backed by gold or any other asset. Instead, it would be backed by the full faith in and credit of the United States government.

In other words, our Digital Dollar would be a computerized version of something we already have.

And for me, this raises a few important questions:

If physical money printing already lowers the purchasing power of the dollar through simple dilution…

How will digital currencies affect inflation?

And how much of a cybersecurity risk do CBDCs pose?

Until these crucial questions and concerns are addressed and resolved, I will remain skeptical of CBDCs.

American free-market experts at The Cato Institute think tank agree and say, “there’s no reason for the federal government to issue a CBDC when the costs are so high, and the benefits are so low. Congress should ensure that the federal government does not issue a CBDC.”

So, the debate rages on.

We live in exciting times where technological innovation has the potential to enhance our lives and make international cooperation more streamlined.

But to help ensure the protection of its citizens, governments must work to ensure that the benefits of CBDCs far outweigh the potential harms.

————————–

Want to learn more about securing your savings with gold? Click here to get a FREE Gold Information Kit or dial toll-free 888-529-0399 now to speak with a Gold Specialist. There’s no cost and no obligation.