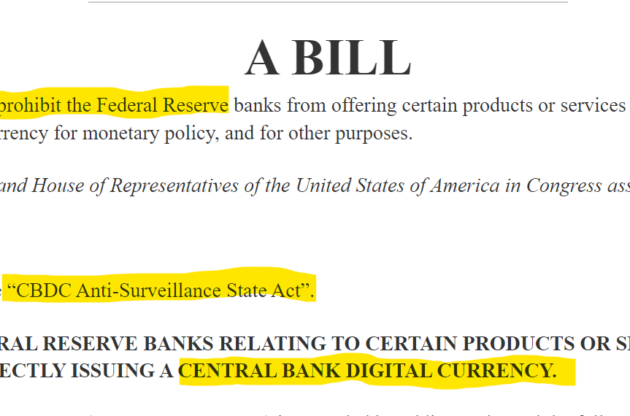

On February 26, 2024, Senator Ted Cruz (R-TX) introduced his version of Representative Tom Emmer’s (R-MN) 2023 “CBDC Anti-Surveillance State Act.”

This is Senator Cruz’s third piece of anti-CBDC legislation. And if passed, the law would “amend the Federal Reserve Act … to prohibit the use of central bank digital currency for monetary policy and for other purposes.”

The lawmakers’ argument?

A digital, programmable currency could potentially end financial privacy while enabling federal overreach.

“The Biden administration salivates at the thought of infringing on our freedom and intruding on the privacy of citizens to surveil their personal spending habits,” says Senator Cruz.

Representative Emmer says CBDCs could be used “as a surveillance tool that Americans should never tolerate from their own government.”

Norbert Michael of the Cato Institute agrees and warns, “It’s not difficult to see that this level of government control is incompatible with both economic and political freedom.”

But are their concerns justified?

Well, here’s the rub:

Unlike paper currency—which is held in independent bank systems—a CBDC would be linked to the Fed’s centralized computers.

Critics say this might give the Fed direct access to citizens’ finances.

And if cash is ever phased out, CBDC opponents say financial privacy may vanish and the central bank may control how citizens use their money.

Bank of International Settlements General Manager Agustin Carstens explains:

“We don’t know who’s using a $100 bill today and we don’t know who’s using a 1,000-peso bill today.

“The key difference with the CBDC is the central bank will have absolute control on the rules and regulations that will determine the use of the expression of central bank liability, and also, we will have the technology to enforce that.”

But advocates say that level of control offers enhanced fraud protection.

Computerized access to the nation’s digital currency, they say, could help catch tax dodgers, money launderers and international terrorists.

And that sounds like a noble pursuit, but you have to wonder…

Wouldn’t sophisticated criminals be aware of CBDC exposure risks and find another way?

And since all financial information would be centralized…

If a cyberattack were to hit the Fed’s computer network, would all the digital currency held by millions of Americans be affected at once?

These potential risks aren’t unique to the US.

Cybersecurity is a growing challenge everywhere.

Yet despite the risks, CBDCs are moving forward worldwide.

According to the Atlantic Council’s CBDC tracker, “134 countries & currency unions, representing 98% of global GDP, are exploring a CBDC.” And “19 of the Group of 20 (G20) countries are now in the advanced stages of CBDC development.”

That includes the US:

“Individual Federal Reserve Banks, including those in New York and Boston, are pursuing CBDC prototypes for both wholesale and retail applications.”

The council also notes, “Treasury Secretary Janet Yellen and Federal Reserve Chairman Jerome Powell have reaffirmed the United States’ interest in a digital dollar.”

But during a March Senate Banking Committee hearing, Fed Chief Powell reassured everyone, “We’re nowhere near recommending—or let alone adopting—a central bank digital currency in any form,” adding, “people don’t need to worry about it.”

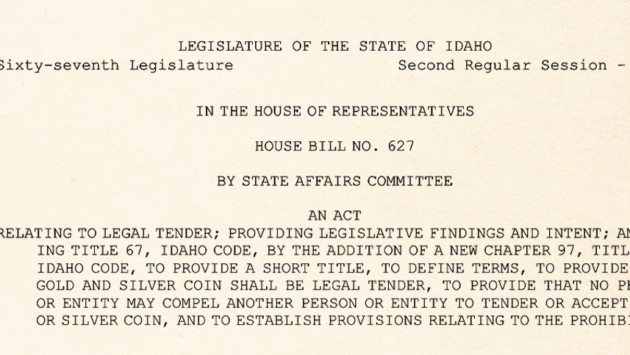

Radical Sound Money Movement Gains Traction in Most US States